A Week of Insight and Inspiration: My Time at the Design Leadership Summit in Toronto

Last week, I had the privilege of attending the Design Leadership Summit in Toronto. This gathering brought...

American Banker Breaks Down Ent Credit Union’s Move into VR Training

Aequilibrium and Motive.io Bring Modern Training Techniques to Ent

Last week, we were honored to be recognized...

Extended Reality (XR) for Credit Unions: Bridging the Digital Gap

Introduction to Extended Reality (XR): The Next Digital Frontier

Extended Reality (XR) – encompassing...

What you Missed at Central 1’s Momentum 2023 Conference

December 7, 2023

Momentum 2023 by Central1, held at the Fairmont Hotel Vancouver from November 27 to...

AEQ as Double Finalists at BCExport 2023

The BC Export Awards stand as a testament to the innovation and success of British Columbia’s export...

Colorado Credit Union Embraces VR for Employee Training with Aequilibrium and Motive.io

Innovative partnership leverages virtual reality to transform professional development in the financial...

VR Training: Explore the Future of Learning

Virtual Reality Has Arrived. For Real.

Virtual reality (VR) has the potential to change so much of what...

6 Ways Unity Unite 2023 Is Shaping the Future of Entertainment and Industrial XR

Unity Unite 2023 in Amsterdam was a pivotal event for XR enthusiasts and professionals. As AEQ continues...

First Impressions of the Meta Quest 3: A Game-Changer in the XR World and Its Impact on Financial Services

The XR landscape has seen tremendous evolution, and the recent release of the Meta Quest 3 only further...

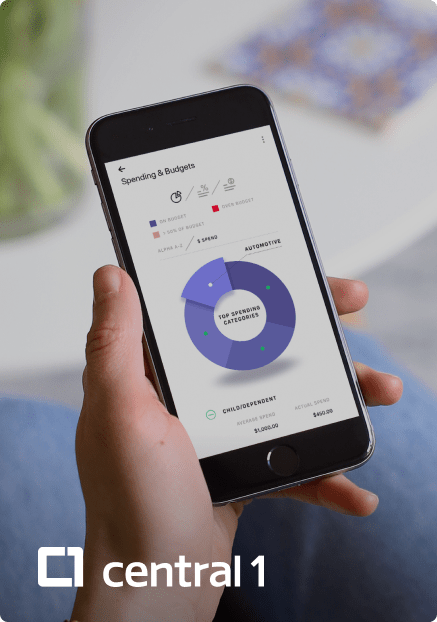

How to Attract Younger Credit Union Members with your Mobile Banking App

Introduction

In an era where the average credit union member’s age hovers around 53, the challenge...